Data source: IPO prospectus

Date: 2017/07/17

I have been reading on this prospectus (total 536 pages) over the last week and entire week end. Netlink is closely related to the industry I'm in, so naturally its IPO attracts my attention.

Given it is one of the largest IPO in the recent years, a lot of financial bloggers have written about their views on its list price of 0.81SGD.

I decided to post my blog only after today's IPO application is closed (at 12pm) so as not to affect anyone's own decision.

The corporate structure is very complicated in this IPO, there are many 'Trust's involved, it is important to understand which and when Trust word is referring to.

To be listed is Netlink NBN Trust (Trust), the underlying business is from Netlink Trust(NLT, another trust, or the original trust). There are two sets of financial statements in prospectus, the audited NLT group's 2015, 2016, 2017 FR; and unaudited pro forma Netlink NBN Trust (Trust)'s 2016, 2017FR. If this has not caused confusion, please refer further to the structure on pg 65.

As IPO subscribers, we are applying to the middle triangle(in dark color)'s units.

As IPO subscribers, we are applying to the middle triangle(in dark color)'s units.

The idea of this complication model, is that NLT (the triangle at the bottom which is actual the original trust that owns the operational biz) is to use this method to be in QPDS(qualified project debt securities scheme), so that IRAS can agree to tax exemption on its interest return(further on this point later, NLT Notes) to Trust(the dark triangle, to be listed)

First thing first, who makes a bulk of money?

Answer: Singtel

In order to be listed, Netlink NBN Trust (Trust) is to acquire from Singtel's portion of NLT(bottom triangle) units with a consideration of SGD$1.8878b(pg 63 notes 1), of which $1.095b paid in cash, with remaining in Trusts(IPO, top triangle) Units: 24.99% (or 966m Units), which is to be held under Singtel Interactive (HoldCo, full subsidiary of Singtel).

I wasn't in Singapore when OpenNet(predecessor of NLT) was setup, so not clear what Singtel's original investment was. But quiet clearly to me, when compare two sets of FR in the prospectus, this action created an intangible asset(goodwill I assume) for Trust, at slight above $1b.

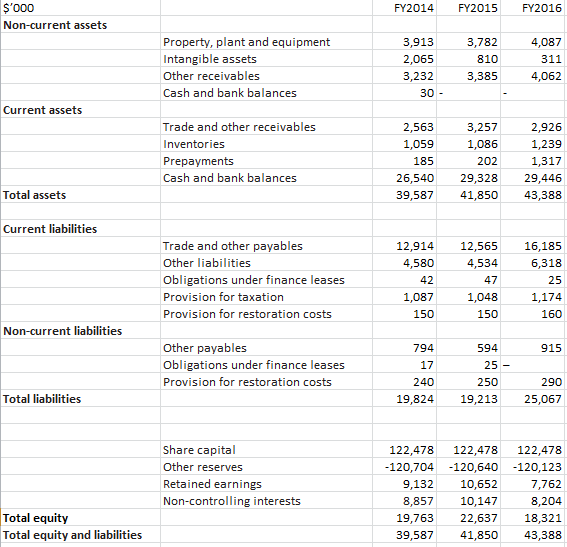

It means: Singtel sold its portion of NLT which is NAV at 0.8878b(1.8878-1) to Trust(IPO we are subscribing to) at $1.8878b, got a cash coffin of over $1b, and 966m Trust Units (at 0.81 per piece) in return.

That is what I call Investment. The goodwill created by this acquisition, will be carried on Trust BS, and amortized over 50years at ~$20m each year.

Trust mgr basically get a piece of business at a higher rate(from Singtel), and then float basically the same biz onto the security market at a lower rate (to NAV, whether due to market condition, other whatsoever reason), of course Trust mgr doesn't have to fork out that short fall(then who?)

Do you go IKEA to get a piece of furniture at 188 and sell it later below 188? Maybe yes, because that is your friend's money, and you get a commission cut from such transaction.

(where is customer's yacht)?

How does TRUST fund its DPU(read as attract its IPO investor)?

The projection is DPU at 5.43% and 5.73% in FY2018, FY2019.

As large CAPEX period is over, depreciation of PPE and amortization of licence/intangible assets etc are largely non-cash items, as long as NLT sets aside enough money for future growth ($211m CAPEX for 2018, 2019 projection) and working capital for daily operation, the remaining(majority) cash generated operationally can be funneled back to Trust, thus allow Trust to distribute all its income to Unit holders.

So much of the fanfare is on an non-SFRS number: EBITDA, a much likened figure of Telecom sector, projected at 240m, 150m for 2019, 2018 respectively, some of which will be the source for NLT to pay Trust.

Of IPO proceeds, $1.1b will be used by NLT to repay its external ST facility agreement, which carries 2.9(or 4+)% interest rate, since Trust is going to help NLT to repay all that ST facility, NLT in term owes 1.1b NLT Notes (pg 119) to Trust(at a rate of 10.5%), a whopping rate jump.

Why would NLT instead of using a ST facility which is at much lower rate, replacing it with NLT Notes to Trust at 10.5%, until 2037?

On the other hand, because IRAS' tax exemption is on the condition that the distribution from NLT to Trust, must be distributed to Trust Unit holders within 3(or 6)mths, thus means interest earned by Trust on NLT Notes, around $110m has to be distributed semi-annually. It is my understanding that this contributes to the 5.43% DPU projection in prospectus; in other words, the actual operationally generated cash for distribution (CAFD) from underlying business of NLT is much smaller.

Should a unit holder rely on DPU based on organic business growth, or based on return of one's own fund (Trust IPO to raise fund from unit holder, pass it to NLT, NLT to repay ST facility, NLT to issue NLT Notes to Trust so as to be QPDS, Trust get interest from NLT and other operating cash income, Trust to distribute cash to unit holder as DPU).

Nonetheless, given fiber is currently already 86% of residential market, and presumably the capex will dwindle down over the years when it reaches saturation, NLT will turn to a cash-cow type of business, with only large depreciation carried on BS, w/o actual cash outflow.

Few things still puzzle me:

- NLT recved $732m in grants for building the nationwide passive fiber infra(amortized at 29m by NLT over 25years). But upon completion of Trust acquisition, this deferred financial support grant will be derecognized at Trust group level. Why? what is the reason this obligation is no longer required?

- Given it is a high regulated market, will IMDA(SG gov) allow NLT(or thus Trust) to earn an abnormally high level of ROI? If not, how can Trust, who relies on NLT business, earn higher return? Without a higher underlying ROI, how does Trust improve DPU? It is further loaded with all the extra structure(thus mgmt fee, commissions, agent fees). Obviously, from another angle, IMDA won't let Trust be in the red, either.

(main revenue contributor, residential connection fee is $13.8/mth, it is revised from previous $15, IMDA review this every 3,5 years, only downtrend foreseeable)

Cut the crap, straight to the point

Whether $0.81 a piece is attractive? Will price go up or down? I have no clue, market price is influenced by many factors, I cannot predict the price movement, especially the short term ones. There are also over-allocation units, stabilization period, lockup commitment to 'stabilize' this big creature.

As I'm really new to such biz trust, my analysis could be error-prone, read with your own care. I myself learnt a lot during this study.

I'll apply some shares(with my own money), I want to keep 100 units to revisit it in 2019. It must be a good learning experience for myself.

Date: 2017/07/17

I have been reading on this prospectus (total 536 pages) over the last week and entire week end. Netlink is closely related to the industry I'm in, so naturally its IPO attracts my attention.

Given it is one of the largest IPO in the recent years, a lot of financial bloggers have written about their views on its list price of 0.81SGD.

I decided to post my blog only after today's IPO application is closed (at 12pm) so as not to affect anyone's own decision.

The corporate structure is very complicated in this IPO, there are many 'Trust's involved, it is important to understand which and when Trust word is referring to.

To be listed is Netlink NBN Trust (Trust), the underlying business is from Netlink Trust(NLT, another trust, or the original trust). There are two sets of financial statements in prospectus, the audited NLT group's 2015, 2016, 2017 FR; and unaudited pro forma Netlink NBN Trust (Trust)'s 2016, 2017FR. If this has not caused confusion, please refer further to the structure on pg 65.

The idea of this complication model, is that NLT (the triangle at the bottom which is actual the original trust that owns the operational biz) is to use this method to be in QPDS(qualified project debt securities scheme), so that IRAS can agree to tax exemption on its interest return(further on this point later, NLT Notes) to Trust(the dark triangle, to be listed)

First thing first, who makes a bulk of money?

Answer: Singtel

In order to be listed, Netlink NBN Trust (Trust) is to acquire from Singtel's portion of NLT(bottom triangle) units with a consideration of SGD$1.8878b(pg 63 notes 1), of which $1.095b paid in cash, with remaining in Trusts(IPO, top triangle) Units: 24.99% (or 966m Units), which is to be held under Singtel Interactive (HoldCo, full subsidiary of Singtel).

I wasn't in Singapore when OpenNet(predecessor of NLT) was setup, so not clear what Singtel's original investment was. But quiet clearly to me, when compare two sets of FR in the prospectus, this action created an intangible asset(goodwill I assume) for Trust, at slight above $1b.

It means: Singtel sold its portion of NLT which is NAV at 0.8878b(1.8878-1) to Trust(IPO we are subscribing to) at $1.8878b, got a cash coffin of over $1b, and 966m Trust Units (at 0.81 per piece) in return.

That is what I call Investment. The goodwill created by this acquisition, will be carried on Trust BS, and amortized over 50years at ~$20m each year.

Trust mgr basically get a piece of business at a higher rate(from Singtel), and then float basically the same biz onto the security market at a lower rate (to NAV, whether due to market condition, other whatsoever reason), of course Trust mgr doesn't have to fork out that short fall(then who?)

Do you go IKEA to get a piece of furniture at 188 and sell it later below 188? Maybe yes, because that is your friend's money, and you get a commission cut from such transaction.

(where is customer's yacht)?

How does TRUST fund its DPU(read as attract its IPO investor)?

The projection is DPU at 5.43% and 5.73% in FY2018, FY2019.

As large CAPEX period is over, depreciation of PPE and amortization of licence/intangible assets etc are largely non-cash items, as long as NLT sets aside enough money for future growth ($211m CAPEX for 2018, 2019 projection) and working capital for daily operation, the remaining(majority) cash generated operationally can be funneled back to Trust, thus allow Trust to distribute all its income to Unit holders.

So much of the fanfare is on an non-SFRS number: EBITDA, a much likened figure of Telecom sector, projected at 240m, 150m for 2019, 2018 respectively, some of which will be the source for NLT to pay Trust.

Of IPO proceeds, $1.1b will be used by NLT to repay its external ST facility agreement, which carries 2.9(or 4+)% interest rate, since Trust is going to help NLT to repay all that ST facility, NLT in term owes 1.1b NLT Notes (pg 119) to Trust(at a rate of 10.5%), a whopping rate jump.

Why would NLT instead of using a ST facility which is at much lower rate, replacing it with NLT Notes to Trust at 10.5%, until 2037?

On the other hand, because IRAS' tax exemption is on the condition that the distribution from NLT to Trust, must be distributed to Trust Unit holders within 3(or 6)mths, thus means interest earned by Trust on NLT Notes, around $110m has to be distributed semi-annually. It is my understanding that this contributes to the 5.43% DPU projection in prospectus; in other words, the actual operationally generated cash for distribution (CAFD) from underlying business of NLT is much smaller.

Should a unit holder rely on DPU based on organic business growth, or based on return of one's own fund (Trust IPO to raise fund from unit holder, pass it to NLT, NLT to repay ST facility, NLT to issue NLT Notes to Trust so as to be QPDS, Trust get interest from NLT and other operating cash income, Trust to distribute cash to unit holder as DPU).

Nonetheless, given fiber is currently already 86% of residential market, and presumably the capex will dwindle down over the years when it reaches saturation, NLT will turn to a cash-cow type of business, with only large depreciation carried on BS, w/o actual cash outflow.

Few things still puzzle me:

- NLT recved $732m in grants for building the nationwide passive fiber infra(amortized at 29m by NLT over 25years). But upon completion of Trust acquisition, this deferred financial support grant will be derecognized at Trust group level. Why? what is the reason this obligation is no longer required?

- Given it is a high regulated market, will IMDA(SG gov) allow NLT(or thus Trust) to earn an abnormally high level of ROI? If not, how can Trust, who relies on NLT business, earn higher return? Without a higher underlying ROI, how does Trust improve DPU? It is further loaded with all the extra structure(thus mgmt fee, commissions, agent fees). Obviously, from another angle, IMDA won't let Trust be in the red, either.

(main revenue contributor, residential connection fee is $13.8/mth, it is revised from previous $15, IMDA review this every 3,5 years, only downtrend foreseeable)

Cut the crap, straight to the point

Whether $0.81 a piece is attractive? Will price go up or down? I have no clue, market price is influenced by many factors, I cannot predict the price movement, especially the short term ones. There are also over-allocation units, stabilization period, lockup commitment to 'stabilize' this big creature.

As I'm really new to such biz trust, my analysis could be error-prone, read with your own care. I myself learnt a lot during this study.

I'll apply some shares(with my own money), I want to keep 100 units to revisit it in 2019. It must be a good learning experience for myself.